Are we addressing the vulnerability of Indian consumers?

- Avishek Saha

- Nov 3, 2025

- 1 min read

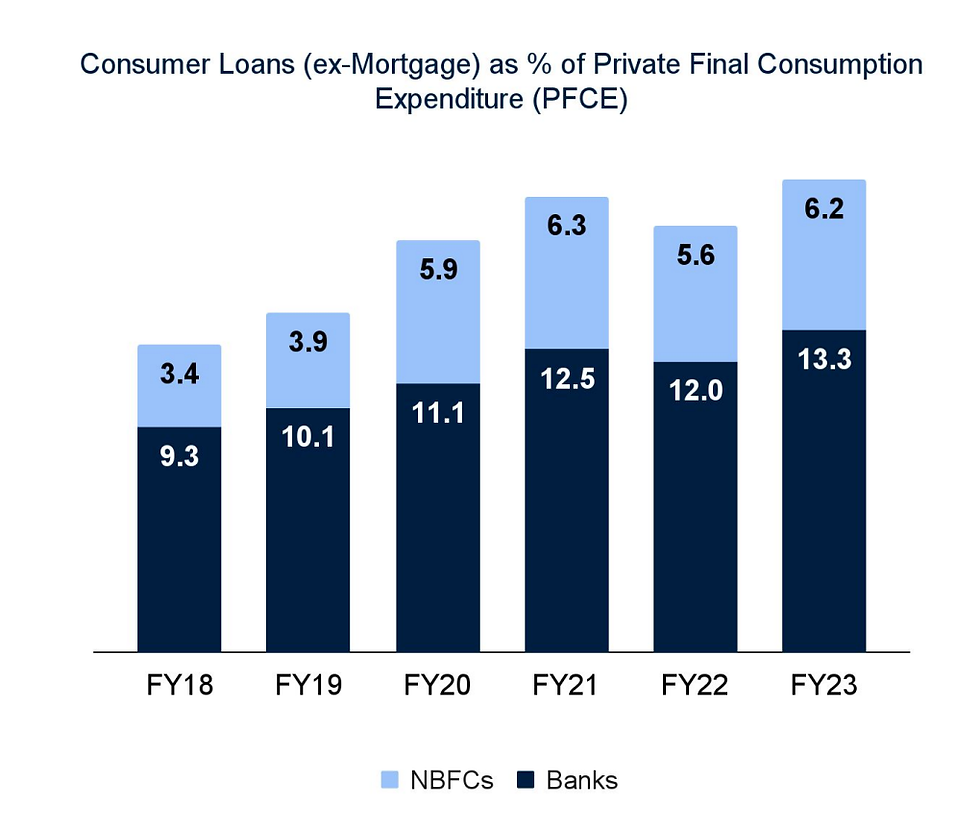

In the last decade, India has seen a sharp rise in credit dependency among consumers. Since FY2012, consumer loans as a percentage of private final consumption expenditure have nearly doubled to 19.5%.

On the surface, this reflects greater access to credit and aspirations driving consumption. But dig deeper, and an unsettling trend emerges: the growth rate of private final consumption expenditure has been consistently slowing down since FY22.

What does this mean?

- More households are relying on debt to sustain their lifestyle and essential expenses.

- Consumption growth is cooling despite higher leverage, signaling pressure on disposable incomes.

- Rising vulnerability: in the event of income disruption, job loss, or health emergencies, households could find themselves trapped in financial stress.

India’s consumer economy is entering a phase where financial resilience matters as much as financial inclusion.

The question we need to ask is: Are we building the right safeguards — through insurance, protection products, and responsible lending practices — to shield consumers from this growing vulnerability?

It’s not just about expanding credit access anymore; it’s about protecting the backbone of our economy — the Indian consumer.

Comments